Chicago #1: The Merchants Who Invented Modern Finance

In April 1848, 82 Chicago merchants founded the Chicago Board of Trade (CBOT), creating standardized grain grading and futures contracts that became the foundation for CME Group's $846 trillion global derivatives market.

How 82 Merchants in a Flour Store Attic Built the Foundation for an $850 Trillion Market

Also available on YouTube & Spotify.

CHICAGO

THE UNSUNG NEXUS OF INNOVATION

This midwest metropolis hosts some of America's most significant but least-celebrated financial institutions. CME Group, the derivatives exchange few outside finance can name, hovers around a $106 billion market cap and generated a record $6.5 billion in revenue in 2025. JPMorgan paid $58 billion for Bank One, bringing Jamie Dimon to Chicago and creating America's largest bank. The global derivatives market now exceeds $846 trillion.

Yet somehow, Chicago remains invisible in the tech world. No "Chicago Mafia" thinkpieces. Minimal podcast deep-dives. The city that essentially invented the infrastructure underpinning modern finance gets less coverage than Austin.

How did Chicago become such an unsung nexus for American innovation?

The answer traces back 177 years to a single week in April 1848, when 82 merchants unwittingly invented the blueprint for every financial exchange, clearing house, and trading platform in existence today.

Over the coming months, we will explore the story of how Chicago became the invisible capital of global finance, a sleeper market for venture capital, and why the patterns those 82 merchants pioneered still drive billion-dollar outcomes today.

ACT I:

THE STORY

The Crisis Nobody Saw Coming

101 South Water Street, Chicago, April 3, 1848. Eighty-two men climbed up the narrow stairs to a flour store attic. The twin odors of crushed grain and dank river moss hung heavy in the air. Outside, the Chicago River carried the spring runoff from melting prairie snow. The same river that had carried a paltry 78 bushels of wheat to Buffalo ten years earlier now handled nearly 2 million bushels annually, a 25,000x increase. However, the infrastructure of trust hadn’t kept pace.

Every transaction was bespoke. A farmer from DeKalb County would arrive with wheat. Was it dry? Moldy? Mixed with oats? Nobody could verify. A merchant would offer a price based on his own inspection. The farmer, needing cash immediately, had no recourse. Wheat that sold for $1.50 per bushel in the morning might fetch 60 cents by afternoon if ships from Milwaukee arrived unexpectedly. Merchants went bankrupt honoring forward contracts when prices spiked. Farmers destroyed crops rather than pay transport costs exceeding grain value.

The Panic of 1837 had already shown Chicago’s vulnerability. When New York banks stopped specie payments on May 10—just eight days after William Butler Ogden’s election as Chicago’s first mayor—the contagion spread instantly. Illinois went bankrupt. The Illinois & Michigan Canal, Chicago’s economic lifeline under construction since 1836, stopped work. Land that sold for $22,000 per lot at the peak reverted to the government for unpaid taxes.

By early 1848, recovery was underway but fragile. And three converging forces were about to flood Chicago with either opportunity, or chaos.

The Conversation That Changed Everything

Thomas Richmond walked into William L. Whiting's South Water Street office in early March 1848 with more than warnings. He had a solution.

Richmond owned grain warehouses. Whiting was Chicago’s premier grain broker, the man Eastern buyers trusted. He’d built that trust through personal relationships and his own capital, often guaranteeing quality with his own money when disputes arose. But that model couldn’t scale.

“The canal opens in weeks,” Richmond said. “We’ll see ten times the grain we handle now. Maybe twenty times.”

Both men understood what the Illinois & Michigan Canal meant. Since 1673, when French explorer Louis Joliet recognized that a single portage separated Lake Michigan from the Mississippi River watershed, Chicago’s destiny had been clear: it would become the pivot point between East and West, North and South. The canal would fulfill that destiny.

But infrastructure without organization meant chaos, not commerce.

“What if we formalize the trade?” Richmond proposed. “Create a board, like they have in London. Standard grades. Standard measures. Standard contracts.”

Whiting saw it immediately. Standardization would transform grain from unique lots requiring individual inspection into fungible commodities tradeable by grade. Warehouse receipts would be as good as cash and could become negotiable instruments. Forward contracts could be honored because “Number 2 Winter Wheat” would mean the same thing to everyone.

They called a meeting for March 13, 1848, inviting the city’s leading merchants. The response was immediate as everyone understood the crisis. That meeting produced a resolution and committee. Three weeks later, on Monday, April 3, eighty-two merchants met above Gage & Haines Flour Store to formally establish the Chicago Board of Trade.

The CBOT Founders

The founding members represented Chicago’s entire commercial ecosystem—and their dynasties would shape the city for generations.

George Smith, the Scottish banker from Aberdeen, controlled three-quarters of Chicago’s currency through his banking network by 1854. His paper money, known as “George Smith’s money,” was more trusted than government notes. The merchants elected him president, but he declined to serve while accepting the honor.

Gurdon Saltonstall Hubbard had arrived in Chicago thirty years earlier as a sixteen-year-old fur trader. The Potawatomi named him “Pa-pa-ma-ta-be”—Swift Walker—after he walked 75 miles overnight to warn Danville of a raid. He’d built Chicago’s first warehouse (critics called it “Hubbard’s Folly” for its ambitious size), first meat packing plant, and first insurance underwriting business.

Joseph Turner Ryerson, the Connecticut iron merchant, had relocated from New Jersey in 1842. His company, J.T. Ryerson & Son, would become Joseph T. Ryerson & Son in 1871, then Ryerson Steel in 1935. The family business lasted 165 years in Chicago steel before merging.

Matthew Laflin arrived from Massachusetts in 1837 with gunpowder manufacturing expertise. He supplied explosives for canal construction and the nascent railroad industry. Later, he built Chicago’s first modern stockyards. His wealth funded Laflin Hall at the University of Chicago.

Thomas Dyer, a Connecticut merchant who’d arrived in Chicago in 1835, became the first serving president. Charles Walker—the man whose 78 bushels started everything—became vice president.

Their constitution established membership fees, trading rules, dispute arbitration, and crucially, the framework for standardized grading. No government subsidy. No venture capital. Just merchants pooling resources to solve a collective problem.

Relationships by business, family, political, and infrastructure ties

The Convergence Week

What makes April 1848 extraordinary isn’t just the CBOT founding. It’s the convergence.

Three days after the founding meeting, on April 6, 1848, telegraph lines reached Chicago from New York via Detroit. For the first time, Chicago merchants could know Eastern prices the same day—not two weeks later by mail.

Seven days after the founding, on April 10, 1848, the Illinois & Michigan Canal officially opened. The General Fry arrived from the Mississippi watershed, completing the water route from New York to New Orleans through Chicago.

Canal. Telegraph. Exchange. All within one week.

This pattern of infrastructure convergence creating winner-take-all advantages explains why Chicago, not St. Louis, became the financial center of the Midwest. St. Louis had superior river geography on the Mississippi but missed the canal-telegraph-exchange convergence by more than two decades. By the time St. Louis caught up, Chicago's network effects were unassailable.

The 82 merchants had positioned themselves at the exact moment when infrastructure made standardized trading possible—and necessary. They didn’t create the convergence. They captured it.

Exchange. Telegraph. Canal. All within 7 days.

The Infrastructure Stack

What happened in that attic wasn’t the founding of a commodity exchange. It was the invention of standardization as infrastructure—the radical idea that defining common grades, measures, and terms creates more value than the transactions themselves.

The merchants built in layers:

1856: Standardized Grading. CBOT established three official wheat categories (White Winter, Red Winter, and Spring) each with precise moisture, weight, and contamination specifications. For the first time, buyers could purchase grain by grade without inspecting every bushel. The USDA's Federal Grain Inspection Service confirms that CBOT enacted the first grain grading rules for U.S. grain in 1856. Impact: a bushel of "Number 2 Winter Wheat" from any Chicago warehouse became interchangeable with any other, collapsing the cost of price discovery overnight.

1859: Self-Regulatory Authority. The Illinois legislature granted CBOT a corporate charter with quasi-juridical powers: authority to set rules, resolve disputes, and expel members. This public-private partnership model became the template for every major exchange. Impact: the charter gave CBOT enforcement power that no purely private contract could replicate, building trust across state lines.

1865: Standardized Futures Contracts. CBOT formalized "to-arrive" contracts with fixed delivery dates, margin requirements, and standardized terms. Farmers could lock in prices months before harvest. Speculators accepted price risk in exchange for potential profit. Hedging at scale became possible. Impact: for the first time, agricultural risk could be separated from agricultural production, allowing capital to flow to whichever party was best equipped to bear it.

Each layer enabled the next. Standardized grades enabled warehouse receipts. Warehouse receipts enabled futures contracts. Futures enabled clearing houses. The infrastructure compounded.

By 1855, the system had earned international trust: the French government purchased grain from Chicago rather than New York, recognizing Chicago's grading system as more reliable.

ACT II:

ANALYSIS

The Geography of Market Infrastructure: Why Chicago Won

The 82 merchants didn't know they were capturing a once-in-a-century convergence. But looking back, we can see exactly why a) Chicago was the only place this could happen in the United States; and, b) why their solution became the operating system for global finance.

Markets require three essential elements that Chicago uniquely possessed in 1848. Understanding these elements explains not just CBOT's success, but why exchanges operate as "stagehands of capitalism"—invisible infrastructure without which the entire show stops.

Element 1: Why Markets Form Where They Do

Financial analyst Byrne Hobart explains why markets cluster at specific geographic points: ports and entrepôts—places where bulk imports get sorted and parceled to specific destinations. That sorting business creates local expertise in grading and comparing product variants.

Chicago in 1848 was the ultimate entrepôt. Grain flowed in from hundreds of prairie farms, each with different moisture content, kernel quality, and contamination levels. It needed to be graded, stored, and redirected to Buffalo, New York, Boston, eventually Europe. The physical infrastructure required for sorting was identical to the infrastructure required for a futures exchange: storage facilities, inspection systems, communication networks, transportation access.

Chicago built the entrepôt first. The financial exchange was a natural extension. This geographic logic also explains why major exchanges remain tied to their original locations even after going fully electronic. CME Group's central timezone enables simultaneous access to Asian market close and European market open. O'Hare's position as the world's busiest airport by aircraft movements enables physical presence when needed. The 40-50% lower costs versus coasts enable companies to achieve profitability faster.

Geographic advantages don't disappear—they evolve.

Element 2: The Fungibility Breakthrough

The genius of CBOT's grading system was making wheat fungible. Interchangeable within grades. Before standardization, every lot was unique. After, "Number 2 Winter Wheat" from any warehouse was identical to "Number 2 Winter Wheat" from any other.

When grain became fungible, three things happened:

Price discovery accelerated. Instead of negotiating each transaction individually based on physical inspection, buyers and sellers could reference a single price for each grade. Information flowed faster. Capital allocated more efficiently.

Transaction costs collapsed. A farmer no longer needed to transport physical grain to find a buyer. Warehouse receipts became negotiable instruments, tradeable like currency. Buyers trusted the grade. Sellers sold to the market, not to specific counterparties.

Speculation became possible. Once grain was fungible, traders could take positions without owning physical inventory. This attracted capital from people who would never touch an actual bushel of wheat but had views on price movements. More participants meant deeper liquidity. Deeper liquidity meant tighter spreads. Tighter spreads attracted more participants.

The virtuous cycle had begun. The merchants who created fungibility captured its value. CBOT membership became worth more than most Chicago real estate.

Element 3: Liquidity Providers Warehouse Risk

The third essential element: intermediaries willing to provide liquidity. "If there's an intermediary who can temporarily warehouse the product in question, it's an easier product to trade," Hobart notes. Markets need participants who are "more time- than price-sensitive" and can provide a good living to "price-sensitive liquidity providers that are willing to hold risk on their books for a while."

Chicago's grain merchants, by default, had goods in their inventory and risk they wanted to take off their books. They were natural liquidity providers.

Every merchant faced the same problem: They'd buy grain from farmers (going long physical grain) and needed to sell it to Eastern buyers (going short). But buyers and sellers didn't arrive at the same moment. Merchants needed to hold inventory, which meant holding price risk. A sudden drop in grain prices could wipe out thin margins.

CBOT's futures contracts let merchants hedge this risk. A merchant who bought physical grain could simultaneously sell futures contracts, locking in a spread. The price risk transferred to speculators willing to bet on price movements. The merchant's profit came from the bid-ask spread and logistics, not from commodity price speculation.

This alignment of natural hedgers (merchants and farmers who had physical exposure) with speculators (traders who wanted price exposure without physical handling) created the critical mass needed for a functioning market.

Without CBOT's standardization, Chicago's grain trade would have remained a series of bilateral transactions with high friction, low trust, and no scale. St. Louis, with its superior Mississippi River access, would likely have captured the Midwest's commodity trading infrastructure. The fact that Chicago overtook a city with better natural geography is proof that institutional innovation matters more than physical advantage.

Every successful market since has required these same three elements. When any element is missing, markets fail. When all three align, winner-take-all dynamics emerge. The pattern CBOT pioneered in 1848 scales to every asset class: if you can make something fungible, position yourself at the natural aggregation point, and attract liquidity providers, you can build a multi-generational franchise.

The Chicago Pragmatism Cycle

The three elements above explain why Chicago won. But the 82 merchants created more than a commodity exchange. They created a template that Chicago businesses have followed for 177 years:

The Chicago Pragmatism Cycle:

1) Crisis -> 2) Pragmatic Solution -> 3) Infrastructure Build -> 4) Institutional Compounding.

This is the pattern that distinguishes Chicago's business culture from Silicon Valley's growth-at-all-costs model. Where Valley companies optimize for speed, Chicago companies optimize for survival through volatility.

The 1848 grain chaos created CBOT. The solution wasn't theoretical. It was operational. The merchants didn't write papers about market microstructure. They built the infrastructure to solve an immediate problem, then discovered that infrastructure had value far beyond the original use case.

In derivatives trading, one mistake can wipe you out. You build systems to survive bad days. The Business Breakdowns podcast describes why new exchanges almost always fail: "The industry is littered with the corpses of startup exchanges." Network effects make incumbents nearly impossible to displace. Every new trader who joins makes the exchange more valuable for the next trader. Every new contract listed attracts more liquidity. The flywheel accelerates.

CBOT's founding members understood something that modern tech founders often miss: boring infrastructure compounds faster than exciting innovation. Build the standards first. The transactions follow.

ACT III:

SYNTHESIS

The Fire Test

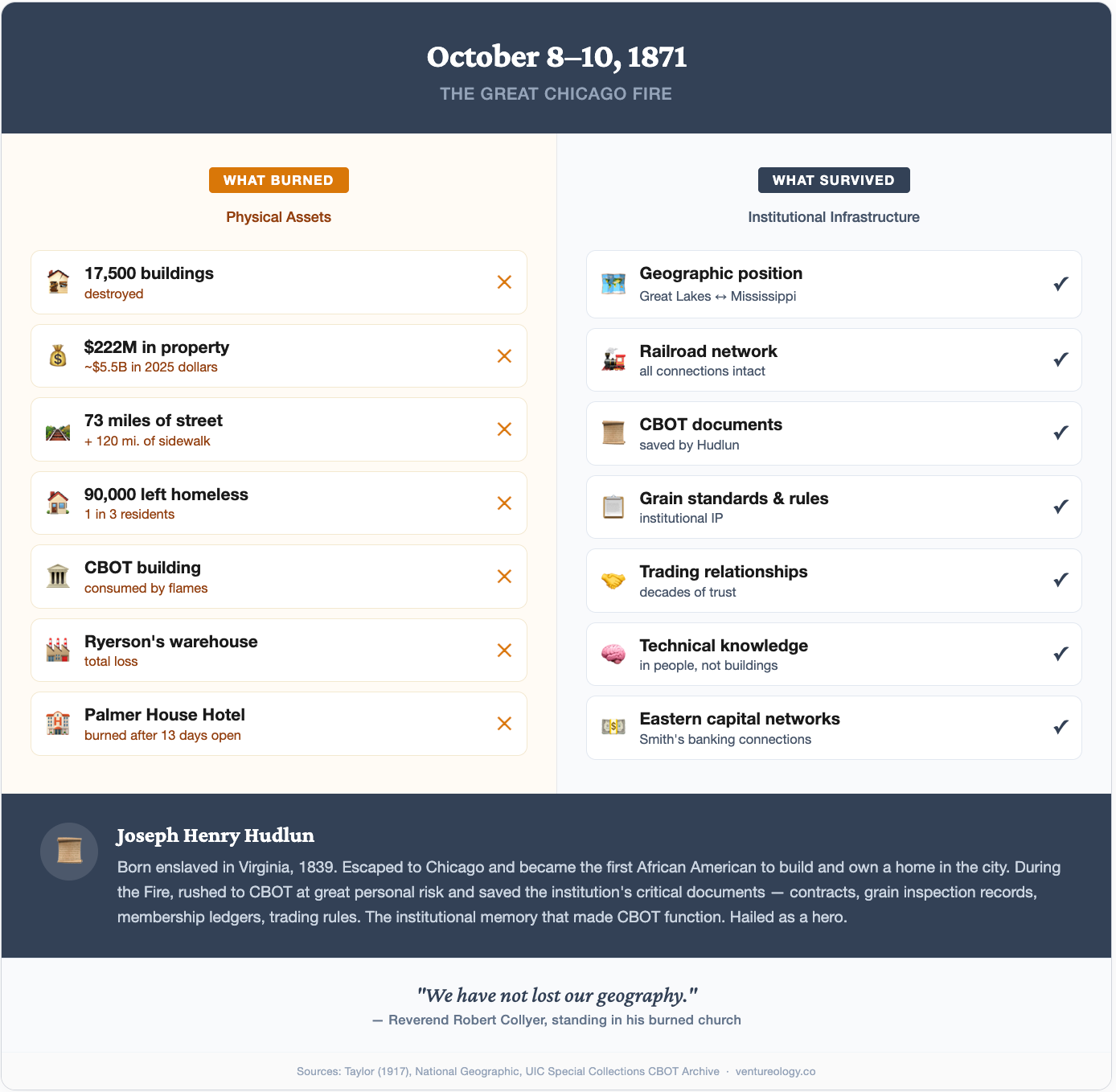

On October 8, 1871, Chicago burned. The Great Fire destroyed 17,500 buildings, left 100,000 homeless, and consumed $222 million in property (~$5.5 billion in 2025 dollars), including CBOT's original building.

Joseph Henry Hudlun, born enslaved in Virginia around 1830, was the first African American to build and own a home in Chicago. He worked at CBOT. When the fire erupted, Hudlun helped his wife tend to the needy, then rushed to the Board of Trade. At great risk to himself, Hudlun saved many of the institution's valuable documents and was hailed as a hero.

What documents were worth risking death to save? Not money. That was insured. The valuable documents were contracts, grain inspection records, membership ledgers, and trading rules. The institutional memory that made CBOT function.

Hudlun understood something profound: destroying those records would destroy trust, and destroying trust would destroy the exchange.

Joseph Ryerson, watching his iron warehouse burn with everything he owned inside, issued a handbill the next morning: "J.T. Ryerson & Co. still lives and will be ready for business as soon as they can find a place."

CBOT's standardization survived the fire. The grades, the contracts, the clearing mechanisms. These couldn't burn. The exchange reopened immediately in temporary quarters. Grain flowed. Contracts cleared. Within 23 months, Chicago was fully reconstructed, stronger, fireproofed, and more systematized than before.

The fire revealed that Chicago's real infrastructure wasn't buildings. It was the standards, relationships, and trust networks the 82 merchants had created. As Reverend Robert Collyer said, standing in his burned church: "We have not lost our geography."

What Survived

The decades following the fire validated everything the founders built. In 1897, Joseph Leiter's failed attempt to corner the wheat market demonstrated that properly structured markets resist monopolization. He lost approximately $20 million (~$750 million in 2025 dollars) trying. The 1920s manipulation scandals led to federal oversight with the Grain Futures Act (1922) and Commodity Exchange Act (1936), formalizing the public-private partnership model still used today.

The pattern the 82 merchants pioneered scaled through open outcry, electronic trading, high-frequency trading, and now algorithmic trading. The technology changed. The infrastructure didn't.

Today, CME Group, the modern successor to CBOT, processes 28.1 million contracts daily, a record annual average set in 2025. Agricultural products still generate over $470 million annually, roughly 11% of CME Group's revenue. Every time you trade a derivative, invest in an ETF, or hedge currency exposure, you're using infrastructure those 82 merchants invented in a flour store attic.

The Template

The CBOT founding established patterns that would repeat throughout Chicago's history:

Eastern capital meets Midwest operations. George Smith's Scottish banking connections funded Chicago's growth. The merchants combined access to capital with operational expertise in logistics and commodities.

Infrastructure convergence creates winner-take-all dynamics. Canal, railroad, telegraph. Whoever captured the convergence point won. St. Louis had better geography but missed the infrastructure timing by 22 years.

Pragmatic problem-solving under crisis pressure builds multi-generational wealth. The Ryerson iron dynasty lasted 165 years. The Laflin fortune seeded the University of Chicago. The exchange itself became the foundation for a $106 billion institution.

Chicago companies still prioritize infrastructure today. Before Braintree (acquired by PayPal for $800 million in 2013) built beautiful payment APIs, they perfected the unglamorous backend of payment processing. Before Uptake (valued at $2.3 billion in 2017) created AI predictions for industrial assets, they built industrial data pipelines.

Chicago's private equity industry, now home to Thoma Bravo ($184 billion AUM), GCM Grosvenor ($86 billion AUM), and dozens more firms, traces its institutional DNA back to relationships built in trading pits and CBOT boardrooms.

The through-line from 1848 to 2026: build infrastructure, create standards, enable markets, compound knowledge, build generational wealth.

Closing

Thomas Dyer died in 1888, age 83, having seen his creation survive its greatest test. The fire revealed that Chicago's real infrastructure wasn't physical. It was the standards, relationships, and institutional trust the 82 merchants had created.

Gurdon Hubbard, the teenage fur trader who became "Swift Walker," died in 1886 at age 84. He'd watched Chicago grow from frontier outpost of 200 people to metropolis of 1.1 million, watched wheat trading evolve from barter to futures contracts, watched his own fortune vanish in the fire and rebuild afterward.

The 82 merchants captured a convergence moment in 1848. Infrastructure plus timing plus institutional innovation. Their solution to grain chaos became the operating system for global finance.

What would those men think of a market that now exceeds $846 trillion in derivatives? Probably this: the abstraction layer between physical and financial that enables modern capitalism traces directly to April 3, 1848, when eighty-two merchants decided standardization was more valuable than any individual transaction.

They were right.

In our next episode, we examine how the 1871 Great Chicago Fire tested everything the 82 merchants built—and how Chicago's response to that crisis established patterns of resilience that distinguish the city to this day.

Episode Index

Key Figures: George Smith (banker, Aberdeen) · Gurdon Saltonstall Hubbard (fur trader, founding member) · Joseph Turner Ryerson (iron merchant, Connecticut) · Matthew Laflin (gunpowder manufacturer, Massachusetts) · Thomas Dyer (first president) · Charles Walker (first vice president, 78-bushel shipment) · William L. Whiting (grain broker) · Thomas Richmond (warehouse owner) · Joseph Henry Hudlun (CBOT employee, document rescuer during Great Fire)

Key Dates: April 3, 1848 (CBOT founding) · April 6, 1848 (first telegraph from the East) · April 10, 1848 (Illinois & Michigan Canal opening) · 1856 (standardized grain grading) · 1859 (Illinois corporate charter) · 1865 (standardized futures contracts) · October 8, 1871 (Great Chicago Fire) · 1897 (Leiter wheat corner attempt) · 1922 (Grain Futures Act) · 1936 (Commodity Exchange Act)

Key Institutions: Chicago Board of Trade (CBOT) · CME Group · Illinois & Michigan Canal · USDA Federal Grain Inspection Service · Gage & Haines Flour Store · J.T. Ryerson & Son

Key Concepts: Fungibility · Standardization as infrastructure · Entrepôt theory of market formation · Chicago Pragmatism Cycle (Crisis → Pragmatic Solution → Infrastructure Build → Institutional Compounding) · Liquidity provisioning · Winner-take-all dynamics · Infrastructure convergence

Primary Sources: Charles H. Taylor, History of the Board of Trade of the City of Chicago (1917, three volumes, commissioned by CBOT) · Encyclopedia of Chicago (Newberry Library / Chicago Historical Society) · USDA Federal Grain Inspection Service · CFTC Historical Archives · Graceland Cemetery Archives · University of Chicago Magazine

Ventureology™ · Chicago Series